Budget & Tax

What drives income tax revenues: Tax rates or economic growth?

Curtis Shelton | April 6, 2021

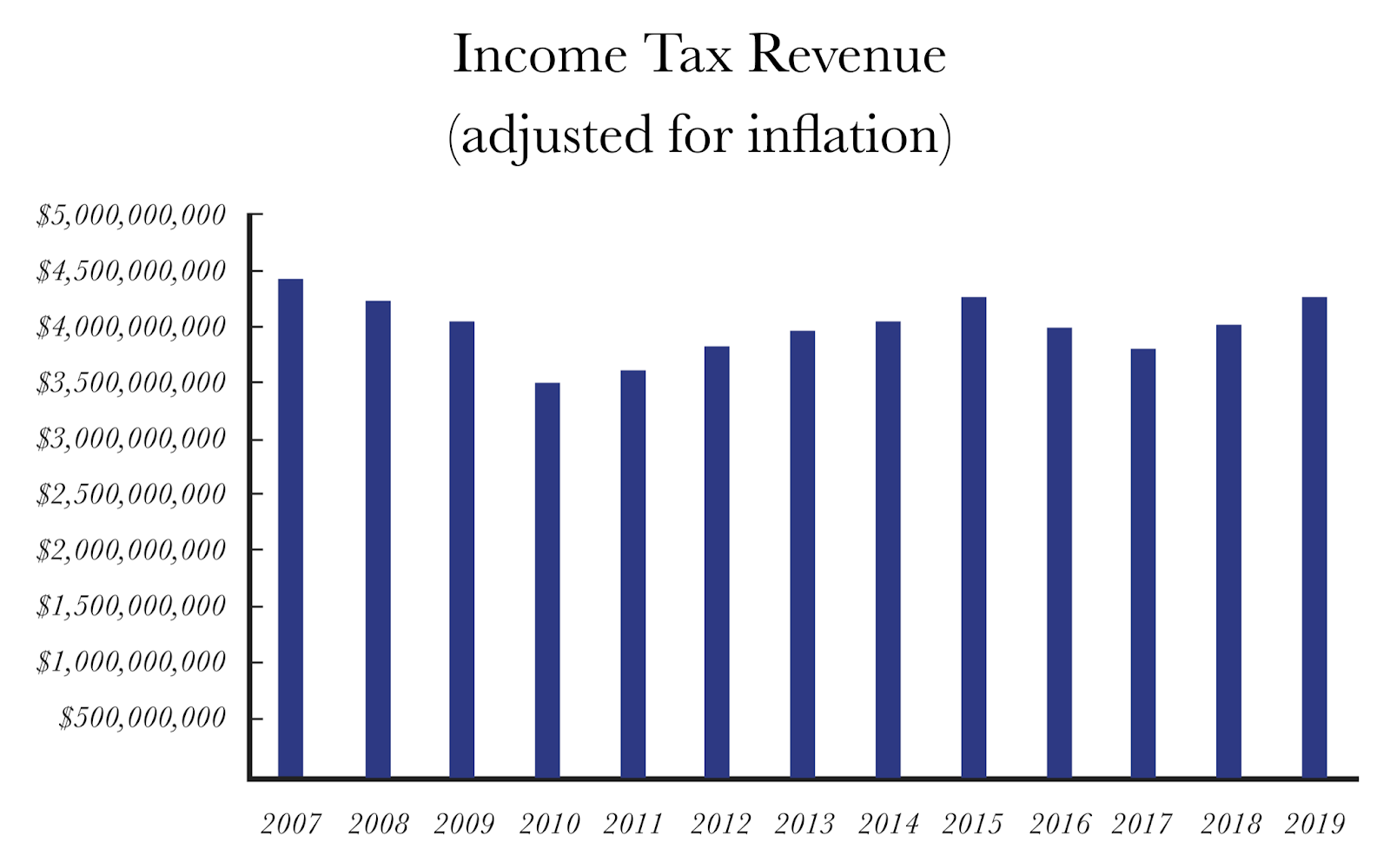

Oklahoma’s marginal personal income tax rate has been reduced to 5% from 5.65% in 2007. Over the next twelve years, revenue from the personal income tax has fallen by $169 million, or 3.8%. Let’s look at the history.

- 2008: reduced from 5.65% to 5.5%

For the next two years, until 2010, there was a dip in revenue. This coincided with the Great Recession as the state suffered a surge in unemployment that peaked at 7% at the beginning of 2010.

- 2012: reduced from 5.5% to 5.25%

After this cut, income tax revenue grew by 11.6% from 2012 to 2015, until the next rate cut in 2016.

- 2016: reduced from 5.25% to 5%

After this cut, the state lost 6.8% in income tax revenue from the prior year, but this also came amid a massive decline in oil prices, an increase in unemployment, and declines in revenue from other taxes. Since then, income tax revenue has climbed to identical levels since the rate cut and is estimated to surpass those prior levels in 2021.

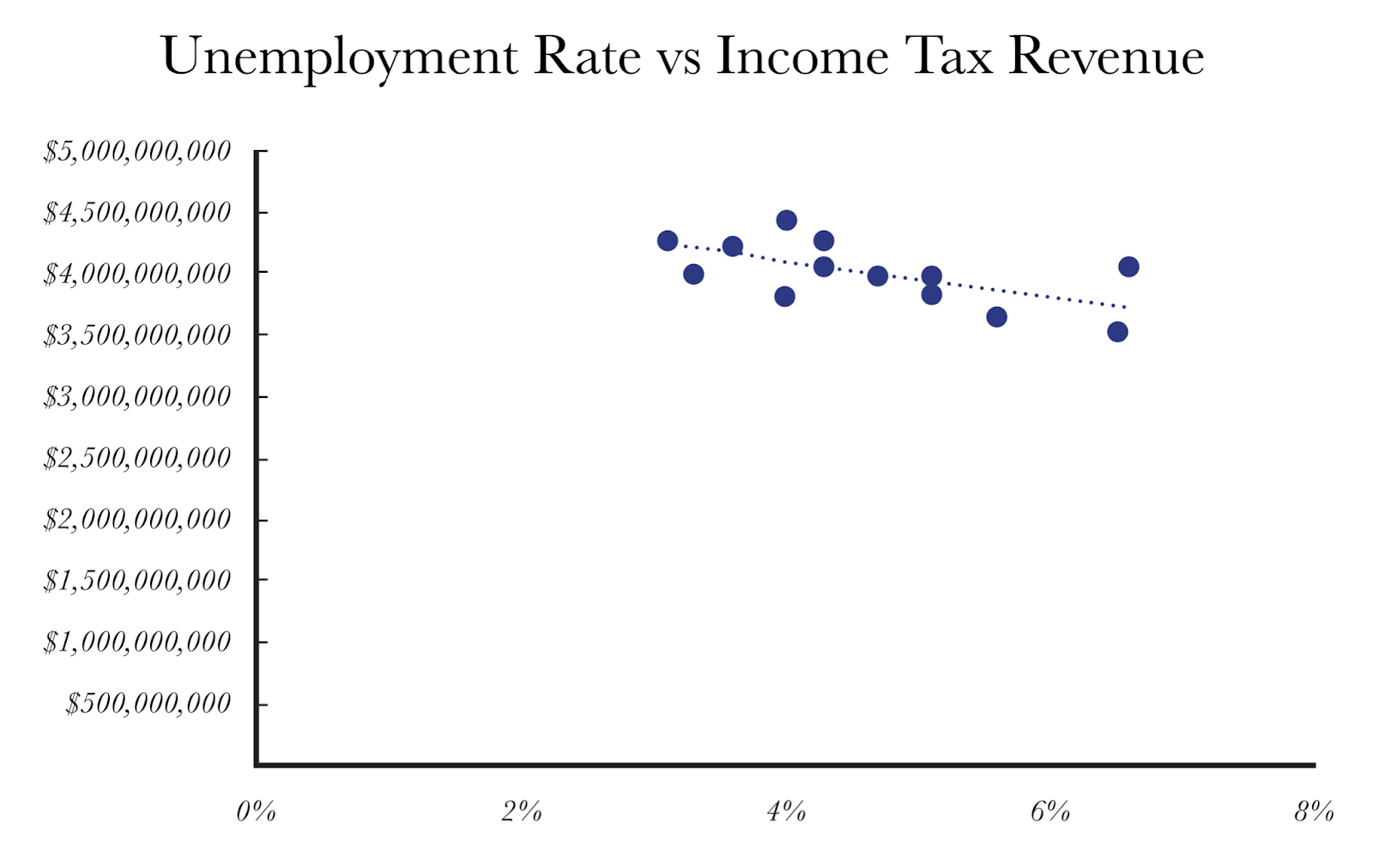

As the charts below indicate, unemployment has a much higher correlation with income tax revenue than does the income tax rate itself. When the state began to recover from economic hardship during each recession, revenue would recover to prior levels—even at a lower tax rate. Policies that encourage the growth of new industries will put Oklahoma in the best position to compete and succeed.

Sources: Oklahoma Tax Commission, Bureau of Labor Statistics, BLS inflation calculator

Curtis Shelton

Policy Director

Curtis Shelton currently serves as the policy director for OCPA with a focus on fiscal policy. Curtis graduated Oklahoma State University in 2016 with a Bachelors of Arts in Finance. Previously, he served as a summer intern at OCPA and spent time as a staff accountant for Sutherland Global Services.